It is also useful for the manager since a complete assessment of the performance for a certain period can be carried out. It allows you to understand what mistakes were made and what should be done to achieve greater efficiency. Founded in 2017, Acgile has evolved into a trusted partner, offering end-to-end accounting and bookkeeping solutions to thriving businesses worldwide. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

- The next step after preparing an Adjusted Trial Balance would be the closing process.

- It makes sure statements like the cash flow are accurate and truly represents the company’s financial health.

- By verifying the equality of debits and credits, the post-closing trial balance confirms that the accounts are ready for the next accounting period.

- Accounting software will generate a post-closing trial balance (or any other trial balance) with a click of the mouse.

- Since these are determined to be temporary accounts, it contains no sales revenue entries, expense journal entries, no gain or loss entries, etc.

Post-Closing Trial Balance Vs. Adjusted Trial Balance:

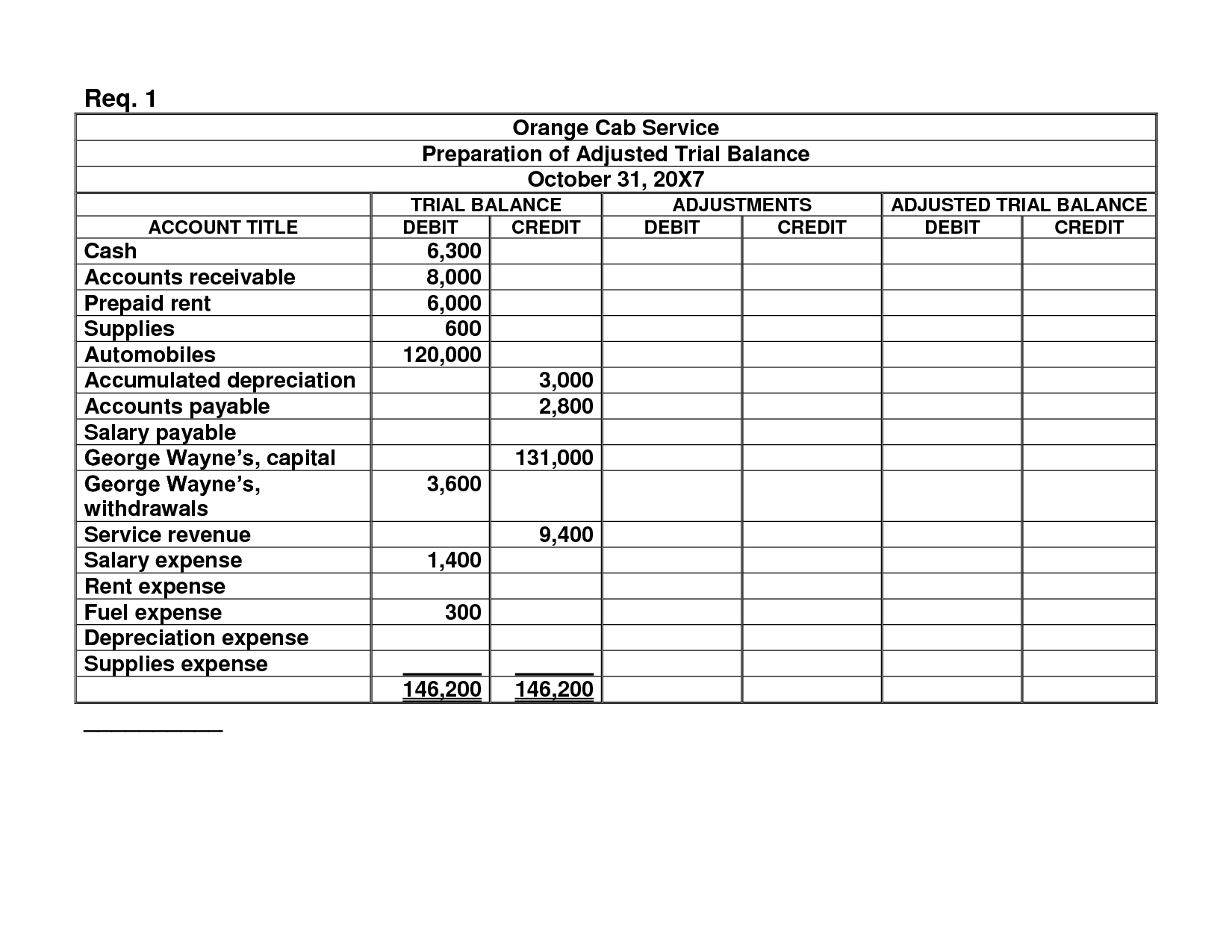

The last step in the accounting cycle (not counting reversing entries) is to prepare a post-closing trial balance. They are prepared at different stages in the accounting cycle but have the same purpose – i.e. to test the equality between debits and credits. The General Ledger Trial Balance Report lists actualaccount balances and activity by ledger, balancing segment, and accountsegment. The report prints the account number, description, and debitor credit balance for the beginning and ending period. The report can print incomestatement, balance sheet, or all balances for a selected range ofaccounting combinations.

AccountingTools

First, identify the accounts that possess balances, and if closing entries were performed correctly, these should simply be those on your company’s balance sheet. It helps to prepare your general ledger for the new accounting period and closes out balances in both expenses and revenue accounts. While it differs from an adjusted trial balance in purpose and content, both serve as crucial tools to ensure the accuracy of financial records and statements. These accounts carry their balances into the next accounting period and are used to prepare the financial statements. However, most businesses can streamline this cycle and skip tedious steps like posting transactions to the general ledger and creating a trial balance. Using accounting software like QuickBooks Online can do all these tasks for you behind the scenes.

Streamline your accounting and save time

Post Closing Trial Balance is the list of all the balance sheet items and their balances, excluding the zero balance accounts. It is used for verification that temporary accounts are properly closed and that the total balances of all the debit accounts and all the credit accounts are equal. A post-closing trial balance is, as the term suggests, prepared after closing entries are recorded and posted. It is the third (and last) trial balance prepared in the accounting cycle. The balances of the nominal accounts (income, expense, and withdrawal accounts) have been absorbed by the capital account – Mr. Gray, Capital.

Role in Verifying Accounting Accuracy

As with the unadjusted and adjusted trial balances, both the debit and credit columns are calculated at the bottom of a trial balance. If these columns aren’t equal, the trial balance was prepared incorrectly or the closing entries weren’t transferred to the ledger accounts accurately. In financial reports, this balance confirms account balances are mathematically correct after closing entries. It makes sure all temporary accounts are cleared, fitting accounting standards. This step keeps the financial statements truthful, including balance sheets and income statements. In both adjusted and unadjusted trial balances, the total of both credit and debit is calculated at the bottom of the trial balance, and they should be equal.

Deferred Tax Assets – Definition, Example, and Why the Deferred Tax Asset Arises

After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. Specify the currency type, such as entered, statistical,or total. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

A trial balance is an internal report that itemizes the closing balance of each of your accounting accounts. It acts as an auditing tool, while a balance sheet is a formal financial statement. It’s one of the first lines of defense against accounting errors and a pivotal report within double-entry bookkeeping.

It’s vital for the adjusted trial balance, pre-closing trial balance, and post-closing trial balance. Knowing their differences improves the value of financial statements. This is to ensure things like dividends are correctly taken from net income.

Temporary accounts are used to record transactions for a specific accounting period, such as revenue, expense, and dividend accounts. A trial balance only contains ending balances of your accounting accounts, while the general ledger has detailed transactions of the accounts. Most accounting software will let you generate a trial balance at any point in time to allow you can i get a tax refund with a 1099 even if i didn’t pay in any taxes to assess the current state of your accounts. Instead, they are accounting department documents that are not distributed. In the next accounting period, the accounting cycle will be repeated again starting from the preparation of journal entries i.e. the first step of accounting cycle. Keeping accurate financial records keeps communication with stakeholders clear.