This agency makes sure the money being sent overseas is not being used to fund terrorist activities or for money laundering purposes. They are also tasked with preventing money from going to countries that are the subject of sanctions by the U.S. government. The agency makes sure the money sent overseas is not being used wire transfer vs electronic transfer to fund terrorist activities or for money laundering purposes.

They can be domestic (between two U.S. accounts) or between a U.S. and an international account.

Some banks offer online tracking through their online banking platform, where you can view the status of the transfer in real-time.

Wire transfers are generally safe and secure, provided you know the person who’s receiving them.

• Wire transfers generally differ from ACH transfers, P2P payments, and checks in terms of speed, fees, and convenience.

If you’re a victim of wire transfer fraud, there’s no guarantee that you can get your money back.

Can you cancel a wire transfer?

Additionally, wire transfers initiated late in the day or during a bank holiday may experience delays as most banks only process transfers during business hours.

While generally secure and reliable, international wire transfers often come with higher fees and longer processing times compared to newer options.

There are many options available these days for sending and receiving money.

Follow the prompts for more details or review Additional Security Feature FAQs for more information.

That coded message authorized the release of funds to the person on the other end. Please be aware that we generate revenue through partnerships with selected money transfer providers listed on our site. Rest assured, these partnerships will not affect your bookkeeping fees when using a money transfer provider, and we guarantee all affiliate providers are trusted and regulated. A hyperlink or a reference to a broker should not be taken as an endorsement of that broker.

What Are the Alternatives to Wire Transfers?

A wire transfer works by transferring funds electronically between banks or financial institutions using secure networks. When you initiate a wire transfer, your bank or transfer service requests the recipient’s banking details, such as their bank account number and SWIFT/BIC code for international transfers. The sender’s bank then forwards these details, along with the amount of money being sent, through a secure network such as SWIFT virtual accountant or Fedwire. International wire transfers, however, can take anywhere from 1 to 5 business days.

Apps and peer-to-peer payment methods

For Remittance Transfers, we’re required by law to inform you of the exact fees that we and/or our agent banks will impose to deliver an international wire. Most of the time you will be able to track it via online portal (be it online banking, or a money transfer service). Banks typically charge both a fixed fee and an exchange rate margin on wire transfers.

When making an international wire transfer, the two costs you will have to look out for are exchange rate markups and fixed transfer fees. Domestic bank wires may take up to three days in the United States, but they are usually much faster, especially if the sender and recipient use the same banking institution. However, human error and other factors can sometimes cause delays, in extreme cases of up to three weeks.

What Is a Wire Transfer? How Does It Work?

These generally take a single business day to complete and are more affordable, with the sender often paying between $15 and $30 and the recipient paying between $0 and $15. Domestic wire transfers are completed when money is transferred from one bank account to another in the same country. International wire transfers are those where the sending and receiving banks are located in different countries. For example, if your U.S.-based bank or credit union sends a wire transfer to a bank in Germany, it’s considered an international wire transfer. The exact fees vary widely depending on the type of payment and the type of bank accounts involved.

For the 2024 tax year, Illinois offers a personal exemption allowance of $2,775 per individual, totaling $5,550 for married couples filing jointly. The 2.11% effective property tax rate in Illinois is second-highest in the nation, behind only New Jersey. That means the typical homeowner in the Prairie State pays 2.11% of their home value in property taxes. The difference between the exemption allowance and the standard deduction is that you can still take it even if you have other subtractions from your income, as mentioned above. With the standard deduction, generally speaking, you have to choose whether to take it or add up your itemized deductions and claim those instead. Your Illinois income includes the adjusted gross income (AGI) amount figured on your federal return, plus any additional income that must be added to your AGI.

Income Tax Brackets, Rates, Income Ranges, and Estimated Taxes Due

Itemized and standard deductions are not allowed in Illinois, which is consistent with the state’s flat tax system. Taxpayers are allowed to claim personal exemptions of $2,375 as of the 2021 tax year—the return filed in 2022. Estimated tax payments are payments of income tax that are required to be paid evenly throughout the year.

Illinois: Federal Retirement Plan Thresholds in 2023

If you (or your spouse if married filing jointly) were 65 or older, check the appropriate box(es). Multiply the number of boxes checked by $1,000 and enter the https://www.bookstime.com/ amount on Line 10b. Illinois’ individual income tax increased from 3.75% to 4.95% on July 1, 2017.

Withholding Income Tax

Illinois also has reciprocity with the neighboring states of Iowa, Kentucky, Michigan and Wisconsin, which means those states don’t tax Illinois residents who work within their borders. So if you live in Illinois and work in Iowa, Kentucky, Michigan or Wisconsin, you’ll pay tax to your home state. The Illinois K-12 education expense credit can knock up to $750 off your tax bill if you spent more than $250 on qualified education expenses. See the instructions for Schedule M to see if you are eligible for other subtractions. To find out if the Illinois Department of Revenue has illinois income tax rate initiated the refund process for your current year refund.

In addition to the Illinois corporate income tax, Illinois corporations must also pay the federal corporate income tax.

Dividend income you received, other than business dividend income, is not taxed by Illinois.

The state’s Schedule M offers a full list of the additions and subtractions that the state recognizes.

However, if you are filing as a resident or a part-year resident, you may be allowed to take a credit against Illinois Income Tax for income tax you paid to another state.

If you received a refund from business taxes, you must include any refund you received as a nonresident to the extent that the original deduction was allocated to Illinois.

Interest income you received while you were a nonresident, other than business interest income, is not taxed by Illinois.

What Income Is Taxable in Illinois

Entities or individuals receiving a pass-through withholding credit or a PTE tax credit receive Schedule K-1-P as a partner or shareholder or Schedule K-1-T as a beneficiary in a pass-through entity. Members may claim credit on their own Illinois income tax return for pass-through withholding reported and paid on their normal balance behalf. Any entity receiving the PTE tax credit that is not itself a pass-through entity, must report the PTE tax credit in the payment section of its own return. If the entity receiving the PTE tax credit is itself a pass-through entity, then the credit is passed through to its members based on each member’s distributive share and reported on Schedule K-1-P or Schedule K-1-T.

Illinois State Taxes: What You’ll Pay in 2025

Schedule K-1-P(3) and Schedule K-1-T(3) are used to calculate the required tax a pass-through entity must report and pay on behalf of its nonresident members that receive business or nonbusiness income from the pass-through entity.

Employers in Illinois must withhold state income tax from employees’ wages based on Form IL-W-4, Employee’s Illinois Withholding Allowance Certificate, and remit these amounts to the Illinois Department of Revenue.

Include earnings distributed from Internal Revenue Code (IRC) Section 529 college savings and tuition programs and ABLE accounts, if these earnings are not included in your adjusted gross income on Form IL-1040, Line 1.

These extensions do not grant you an extension of time to pay any tax you owe.

Instruction how to only prepare a IL state return on eFile.com and then download, print sign and mail it in. Schedule M, Other Additions and Subtractions for Individuals, allows you to figure the total amount of additions you must include on Form IL-1040, Individual Income Tax Return, Line 3 and subtractions you may claim on Form IL-1040, Line 7. Profit and prosper with the best of Kiplinger’s advice on investing, taxes, retirement, personal finance and much more. Residents of Illinois must pay sales tax on items that are tax-exempt in some other states. Profit and prosper with the best of expert advice on investing, taxes, retirement, personal finance and more – straight to your e-mail.

Underpayment can result in penalties based on the amount owed and the number of days late.

Enter the amount of business expenses you deducted this year for which the related compensation is allocable to Illinois.

Investment income—such as interest, dividends, and capital gains—is taxable if reported on a federal return.

According to the Tax Foundation, the average effective property tax rate in Illinois is 1.95%, which is one of the highest rates in the country, and median property taxes are over $5,000.

If you received income from an Illinois trust or estate, that entity is required to send you an Illinois Schedule K-1-T, Beneficiary’s Share of Income and Deductions.

On the state level, you can claim allowances for Illinois state income taxes on Form IL-W-4.

Based on the information provided by the pass-through entity and any other Illinois-based income, you must determine your own Illinois tax liability.

A bigger paycheck may seem enticing, but smaller, more frequent paychecks can make it easier to budget without coming up short by the end of the month. For each pay period, your employer will withhold 6.2% of your earnings for Social Security taxes and 1.45% of your earnings for Medicare taxes. Together these are called FICA taxes, and your employer will pony up a matching contribution. Localities can add as much as 4.75%, and the average combined rate is 8.890%, according to the Tax Foundation. A financial advisor can help you understand how taxes may impact your overall financial goals. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can have a free introductory call with your advisor matches to decide which one you feel is right for you.

Large-cap stocks are more frequently traded and usually represent well-established, stable companies. In contrast, small-cap stocks often belong to newer, growth-oriented firms and tend to be more volatile. Let’s explore more about common stock and how it fits into the big picture of a company’s finances. In recent years, more companies have been increasingly inclined to participate in share buyback programs, rather than issuing dividends. Otherwise, an alternative approach to calculating shareholders’ equity is to add up the following line items, which we’ll explain in more detail soon.

Flexibility in investment strategies

It is also known as net assets since it is equivalent to the total assets of a company minus its liabilities or the debt it owes to non-shareholders. If a company chooses to repurchase some of its common stock, its assets will decrease by the amount of cash it spends even as stockholders’ equity falls by the same amount. The only difference in this case is that the accounting entry for the debit is called “treasury stock.” The inflow of cash increases the cash line in the company balance sheet. To balance out that accounting entry, stockholders’ equity is credited by the same amount.

Preferred Stock vs. Common Stock

Common stocks are the number of company shares that are found on the company’s balance sheet. Common Stockholders are the company’s owners; they earn voting rights and are eligible for dividends. On a company’s balance sheet, common stock is recorded in the “stockholders’ equity” section.

Understanding Capital Stock

Assets are resources that a company owns or controls and that have future economic benefits. They are typically listed on the balance sheet in order of liquidity, meaning the ease with which they can be converted into cash. Examples of assets include cash, accounts receivable, inventory, and property, plant, and equipment.

Trading and Price Changes

The current portion of long-term debt represents the amount of long-term debt that is due within one year from the date of the balance sheet.

The balance sheet is an important financial statement because it provides investors with a snapshot of a company’s financial position.

The balance sheet shows the company’s assets, debts, and the slices owned by investors (equity).

When buying a stock, investors don’t have to wonder exactly what type of stock it is.

The snapshot below represents all the data required for common stock formula calculation. Their voting rights allow them to participate in policy decision-making, elect directors, participate in corporate policies, etc. If it is high, it might be pricey; if it is low, it could be a good deal. Equity stock sales represent one of the most common ways for a company to raise capital.

Common stock represents a residual ownership stake in a company, the right to claim any other corporate assets after all other financial obligations have been met. Assets include what the company owns or is owed, such as its property, accounts receivable journal entries equipment, cash reserves, and accounts receivable. On the other side of the ledger are liabilities, which are what the company owes. If a company is healthy, the total assets will be larger than the total liabilities.

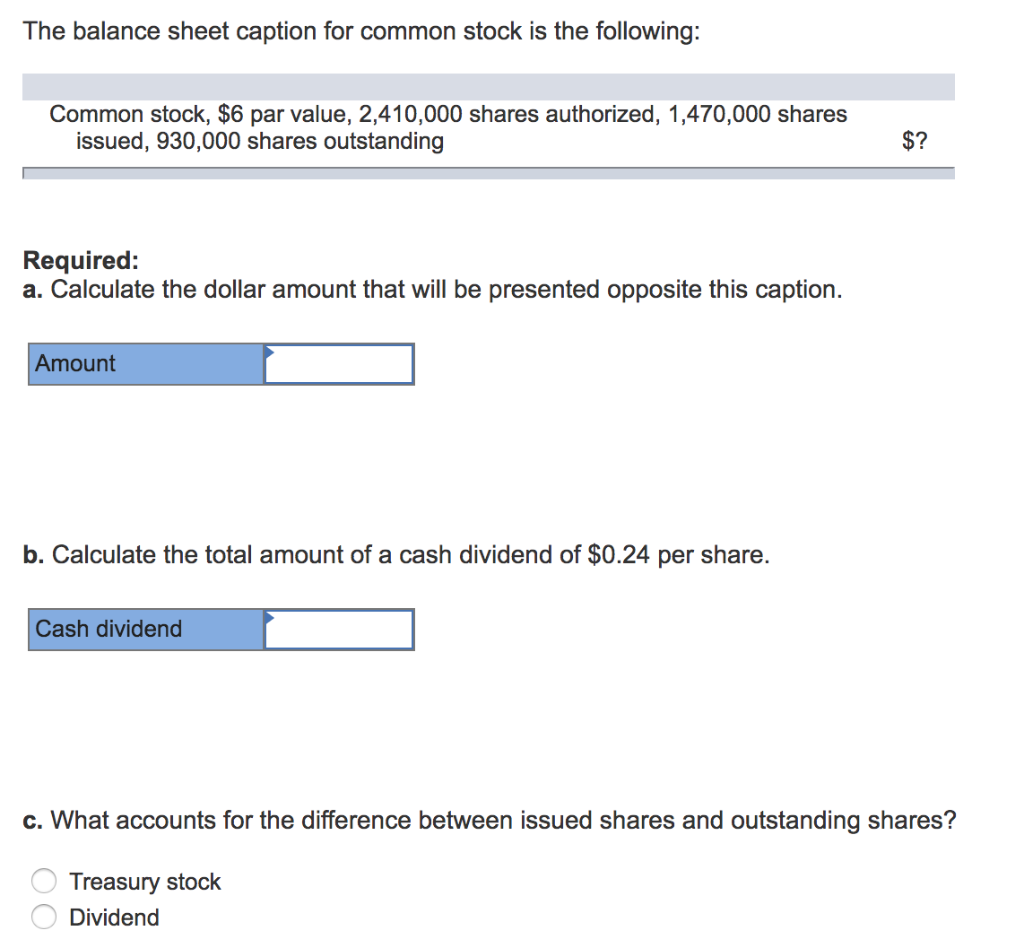

The amount of equity to be issued is $3 per share ($2 is the value of the PAR, and $1 is above the PAR). Now that we have an understanding of what shareholders’ Equity is, we can now show the entry of common stock in a balance sheet in the stockholders’ section of a financial statement. Current liabilities are obligations that are expected to be settled within one year. Examples of current liabilities include accounts payable, wages payable, accrued expenses, and short-term debt. The calculation of common stock on the balance sheet is also important for valuing the company. Investors use the information provided by the balance sheet, including the calculation of common stock, to determine the fair market value of the company and its common stock.

Regularly review your portfolio, track your stocks’ performance, and be ready to make adjustments if necessary. Once you’ve found some promising stocks, decide how much money you’re comfortable investing. A good rule of thumb is to invest only what you can afford to lose, especially when you’re just starting. The stock market can be volatile, so it’s wise to keep a diversified portfolio and not put all your eggs in one basket.

Retained earnings are a company’s net income from operations and other business activities retained by the company as additional equity capital. They represent returns on total stockholders’ equity reinvested back into the company. Public companies, on the other hand, are required to obtain external audits by public accountants, and must also ensure that their books are kept to a much higher standard. Balance sheets allow the user to get an at-a-glance view of the assets and liabilities of the company. In this example, Apple’s total assets of $323.8 billion is segregated towards the top of the report.

Investors trust your numbers, auditors can verify your records faster, and decision-makers have the right data to plan ahead. Without contra accounts, businesses risk financial misstatements that could lead to audits, penalties, or poor strategic choices. Strong financial reporting helps you present a true and reliable picture of your business’s financial health. They prevent overstated revenue, inflated assets, and misleading liabilities, ensuring that your financial statements reflect real values. The frequency depends on the type of transaction and the company’s bookkeeping cycle.

Notes receivables are promissory notes that include a promise from a borrower to repay a lender. The allowance for doubtful accounts is a contra asset because it reduces the value of the accounts receivable (AR) account on the general ledger. Often when a company extends goods on credit, management expects some of those customers not to pay and so anticipates writing off bad debt. Instead of recording deductions as expenses, you track them separately to keep your sales figures accurate.

Contra Asset Examples

The proper size of a contra asset account can be the subject of considerable discussion between a company controller and the company’s auditors. The auditors want to ensure that reserves are adequate, while the controller is more inclined to keep reserves low in order to increase the reported profit level. A contra asset is a negative account used in double-entry accounting to reduce the balance of a paired asset account in the general ledger. It integrates with leading accounting platforms like QuickBooks, Xero, and NetSuite, automatically syncing transactions and receipts.

We strive to empower readers with the most factual and reliable climate finance information possible to help them make informed decisions. Our goal is to deliver the most understandable and comprehensive explanations of climate and finance topics. Carbon Collective is the first online investment advisor 100% focused on solving climate change.

The list of asset accounts on your general ledger and balance sheet conveys the combined, potential value of all of the tangible and intangible items that your organization possesses.

The auditors want to ensure that reserves are adequate, while the controller is more inclined to keep reserves low in order to increase the reported profit level.

As a reminder, assets and expenses are debit accounts whereas liabilities and revenues are credit accounts.

Sometimes, the current value of a note receivable will fall compared to its face value.

Some of the most common contra assets include accumulated depreciation, allowance for doubtful accounts, and reserve for obsolete inventory.

Choosing the right account ensures your financial statements reflect accurate values. A contra-asset account has a credit balance, which lowers the total asset value. A contra-revenue account has a debit balance, reducing total revenue, and a contra-liability account also has a debit balance. Suppose a company estimates that 5% of its $200,000 accounts receivable balance is uncollectible. It records a $10,000 allowance for doubtful accounts by debiting Bad Debt Expense for $10,000 and crediting Allowance for Doubtful Accounts for the same amount. This practice adheres to the matching principle, which requires expenses to be recorded in the same period as the related revenues.

The contra asset account would be used to offset the equipment account on the balance sheet. For example, if the company purchased a computer for 1,000 and it had a five-year life expectancy using straight-line depreciation, the contra account would be debited for 200 each year (the 1,000 divided by 5 years). For example, if you record depreciation, you debit depreciation expense and credit accumulated depreciation in the contra-asset account.

Strengthen your financial reporting with accurate contra accounts

The balance sheet would report equipment at its historical cost and then subtract the accumulated depreciation. A contra liability is a general ledger account with a debit balance that reduces the normal credit balance of a standard liability account to present the net value on a balance sheet. Examples of contra liabilities are Discounts on Bonds and Notes Payable and Short-Term Portion of Long-Term Debt.

Types of Contra Accounts – Explanation

When the original dollar amount is kept in the original account and a separate account is used for recording the deduction, the resulting financial information becomes more transparent and helpful for stakeholders. For example, a building is acquired for $20,000, that $20,000 is recorded on the general ledger while the depreciation of the building is recorded separately. In this article, we’re going on a deep dive into what exactly a contra account is, how contra accounts work, why and how you would use contra accounts and more. And why stop at just theory when you can apply what you’ve learned using premium templates?

They are useful in preserving the historical value in the main account while presenting a write-down or decrease in a separate contra account that nets to the current book value. Contra accounts appear on the same financial statement as the related account. For example, an accounts receivable’s contra account is a contra asset account. This type of account can also be called the bad debt reserve or allowance for doubtful accounts. These accounts adjust assets, liabilities, revenue, and equity without altering the original transactions.

1. Sales Discounts, Returns and Allowances Revenue Contra

We believe that sustainable investing is not just an important climate solution, but a smart way to invest. Angela Boxwell, MAAT, is an accounting and finance expert with over 30 years of experience. She founded Business Accounting Basics, where she provides free advice and resources to small businesses.

In bookkeeping, a contra asset account is an asset account in which the natural balance of the account will either be a zero or a credit (negative) balance.

Below is the asset account debit balance and accumulated depreciation account credit balance on the balance sheet.

All accounts also can be debited or credited depending on what transaction has taken place.

Companies can analyze real financial trends and make informed business decisions by maintaining contra accounts. Managing contra-liability accounts helps you keep your financial records accurate. If you don’t track these adjustments, your liabilities may look higher than they actually are. When you issue bonds at a discount, you receive less money than the bond’s face value.

However, these vehicles have experienced significant wear and tear in the intervening years. And currently, Show-Fleur anticipates that it could only sell each one for roughly $50 thousand, meaning the depreciation per vehicle is $100 thousand. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

The debit balances in the above accounts are amortized or allocated to an expense, such as Interest Expense over the life of the bonds or notes payable. The amount in the accumulated depreciation account is deducted from the assets of a company, such as buildings, vehicles and equipment. This can help anyone viewing the financial information to find the historical cost of the asset. The accumulated depreciation amount shows how much depreciation expense has been charged against an asset.

This article will give you the definition of contra list of contra asset accounts in accounting, talk about different contra accounts, and give examples. Regular reconciliation ensures your contra accounts match actual transactions. This helps you avoid errors, detect fraud, and stay compliant with GAAP (Generally Accepted Accounting Principles). Managing these accounts helps you comply with GAAP, improve financial reporting, and prepare for potential losses.

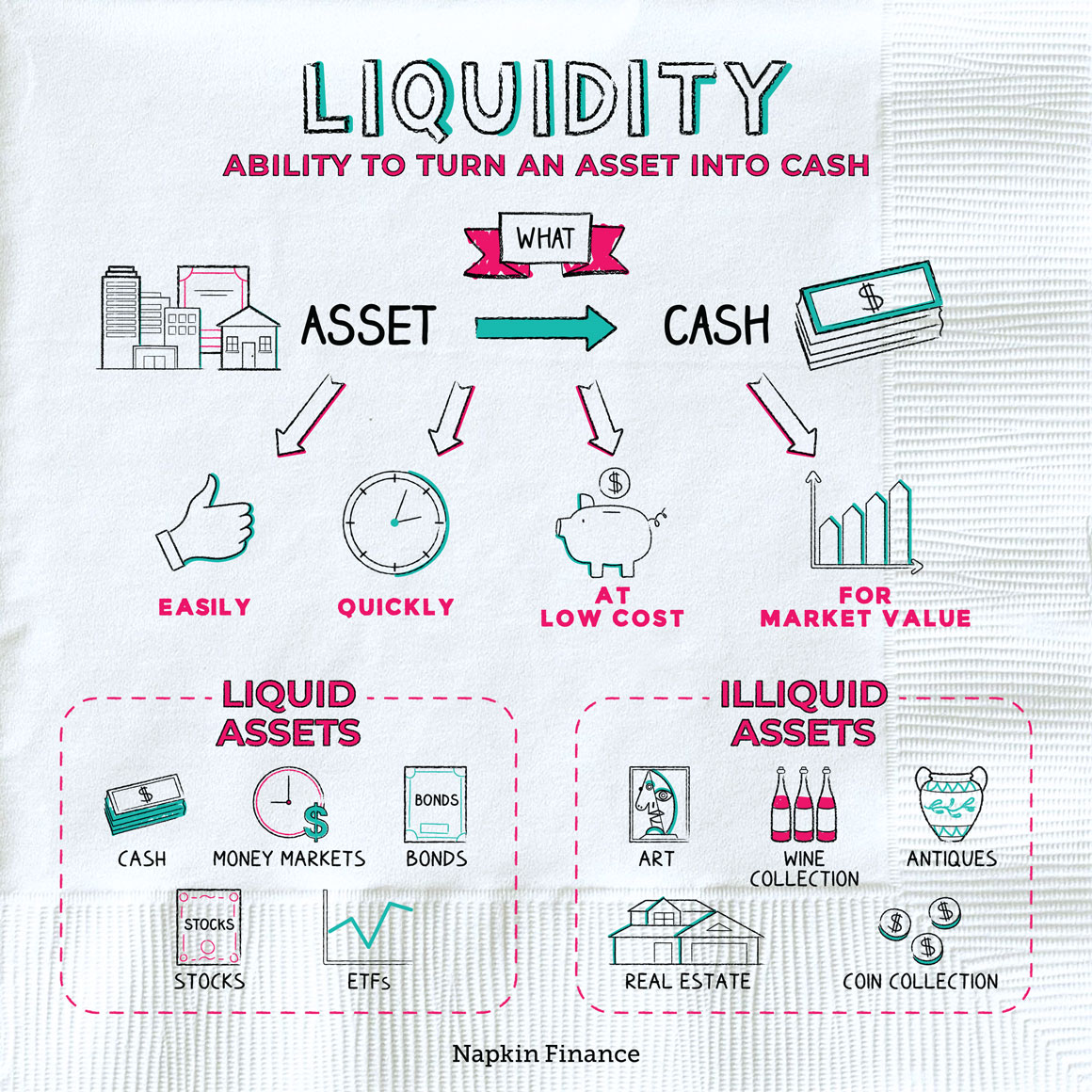

Because they are the most liquid, meaning, you can convert them to cash quickly and easily. Let’s take a look at an example of a balance sheet for a fictional company “ABC Enterprises” to illustrate the order of liquidity. The AI EO addresses everything from advancing AI in healthcare to developing guidance designed to mitigate risks of IP theft. But two of its more consequential provisions — which have raised the ire of some Republicans — pertain to AI’s security risks and real-world safety impacts. High liquidity ensures that firms can make these moves promptly without resorting to lengthy financing processes.

How We Make Money

But this compensation does not influence the information we publish, or the reviews that you see on this site. We do not include the universe of companies or financial offers that may be available to you. The ordering of the items in a balance sheet (assets and liabilities) is called marshalling. In accounting, the term order of liquidity describes the order of decreasing liquidity in which assets are presented in the balance sheet. Understanding the composition and characteristics of other assets is essential for accurately evaluating an organization’s liquidity position and overall financial health.

Quick Links

Conversely, a wide bid-ask spread signifies low liquidity, as there is a significant gap between the prices at which buyers are willing to purchase and sellers are willing to sell. For example, if a company has cash on hand but also holds patents they can sell, the company may decide to sell the patents in order to raise cash quickly. Finally, intangible assets are at the bottom of the list because they are the least liquid and can take longer to convert to cash. A company’s order of liquidity is an important factor to consider when assessing its financial health. Liquidity isn’t just about survival; it empowers strategic agility, enabling timely capitalization on growth prospects and investment opportunities. Liquid firms can swiftly capitalize on promising investment opportunities without the lengthy process of securing external funds.

What is the Importance of Understanding Order of Liquidity in Financial Analysis?

High liquidity is synonymous with a liquid market, where assets can be swiftly bought or sold without causing substantial price movements. On the other hand, low liquidity can lead to price volatility and may result in difficulties in executing trades at favorable prices. Liquidity, in the realm of finance, refers to the degree to which an asset or security can be quickly bought or sold in the market without causing a significant change in its price.

Incorporating order of liquidity considerations in financial modeling can lead to more accurate forecasting of cash flows and better risk management.

Led by editor-in-chief, Kimberly Zhang, our editorial staff works hard to make each piece of content is to the highest standards.

Conversely, a wide bid-ask spread signifies low liquidity, as there is a significant gap between the prices at which buyers are willing to purchase and sellers are willing to sell.

The first thing that comes to mind is petty cash, which is the money a business puts aside to make small purchases on regular basis and it has someone responsible for this petty cash amount.

Which are liquid assets you can convert into cash immediately at the current assets of the market price, through marketable securities.

How Can Order of Liquidity Affect a Company’s Financial Health?

Assets with lower liquidity may offer higher returns, but they also carry a higher risk of not being easily sold in the market. As we embrace the multifaceted nature of liquidity and its order, it is imperative for investors, financial analysts, and market participants to integrate these concepts into their decision-making processes. By doing so, individuals can enhance their understanding of liquidity risk, optimize their portfolio composition, and make strategic investment choices that align with their financial goals and risk appetite. Further down the order of liquidity are assets such as real estate, private equity investments, and certain types of bonds that may have limited trading activity or longer settlement periods. These assets are characterized by lower liquidity, as their conversion into cash may entail longer timeframes, transaction complexities, or the need to find suitable buyers or counterparties. There are various factors that contribute to the liquidity of an asset, including the trading volume, bid-ask spread, market depth, and the presence of willing buyers and sellers.

Bankrate logo

While the advantages of liquidity encompass flexibility, risk reduction, and seizing opportunities, potential risks include limited investment options and opportunity costs. This metric offers a more stringent assessment of a company’s short-term liquidity, as inventories may not be as readily convertible to cash as other assets. A financial crisis might be exacerbated when institutions lack funding liquidity, as they might resort to selling assets en masse, further driving down prices and creating a vicious cycle. Operational costs such as payroll, raw material purchases, and utility bills require liquid assets.

For an individual, this could mean owning a house outright but not having the cash to cover utility bills and student loan payments. If your only assets are your house and car — both illiquid assets — you have liquidity risk. For example, if a company needs to carry out a large purchase within 30 days, but most of its assets are tied up in long-term investments, the company would have liquidity risk. Well, marketable securities such as stocks, bonds, ETFs and mutual funds are typically considered liquid because they can often be sold or traded quickly.

Promptly collecting receivables, negotiating favorable payment terms with suppliers, and optimizing inventory levels can free up cash, enhancing liquidity. These tools grant companies the ability to draw funds when needed, enhancing their liquidity position without holding excess cash reserves. This involves diligent monitoring of inflows and outflows, ensuring timely collections, delaying unnecessary expenses, and leveraging technology for cash flow forecasting. Market liquidity refers to liquidity within an entire market, such as the stock market or real estate market. Securities like stocks or other publicly traded financial assets fall somewhere along the middle of the liquidity spectrum.

It permeates the core of financial markets, influencing market integrity, risk management practices, and the overall resilience of the financial system. Liquidity is a fundamental concept in finance, referring to the ease with which an asset can be converted into cash without significantly impacting its market price. In simpler terms, it measures how quickly and efficiently an asset can be bought or sold in the market. Assets with high liquidity can be easily traded, while those with low liquidity may encounter challenges in finding buyers or sellers at a desired price. Aggregated order books function by pulling data from various exchanges and liquidity providers, combining all available buy and sell orders into one unified feed.

Thus, the stock for a large multinational bank will tend to be more liquid than that of a small regional bank. The most liquid stocks tend to be those with a great deal of interest from various market actors and a lot of daily transaction volume. Such stocks will what does order of liquidity mean also attract a larger number of market makers who maintain a tighter two-sided market. In addition to trading volume, other factors such as the width of bid-ask spreads, market depth, and order book data can provide further insight into the liquidity of a stock.

When analyzing financial statements, goodwill considerations are essential as they impact the overall net worth and value of a company. Understanding and assessing goodwill allows investors and stakeholders to gauge the true value of a business beyond its physical assets. In terms of liquidity assessments, goodwill can affect a company’s ability to generate cash flow and meet short-term obligations, making it a critical component in financial decision-making processes.

They rely on retail banks for convenient and accessible banking solutions, allowing them to manage their money and make payments smoothly. Retail banks also impose lower lending limits, restricting access to substantial capital for large projects or investments. According to a 2022 report by the Federal Reserve (Fed), small businesses often face challenges securing loans above $1 million from retail banks due to these limitations. In contrast, commercial banks specialize in higher loan amounts and tailored credit solutions, making them better suited for corporate clients. This difference highlights the gap between personal banking and business-oriented financial services. In summary, retail banks primarily generate revenue through interest income from consumer lending, fees, and non-interest income from investment products.

Retail banking primarily caters to individual customers, offering tools like savings accounts, debit cards, and transactional support.

Credit cards allow customers to borrow funds for everyday expenses, while small consumer loans finance purchases like appliances or home renovations.

Retail banks provide a wide array of financial services to meet the individual needs of their customers.

Understanding their differences helps individuals and companies make informed decisions for financial growth and success.

These benefits reflect the customer-centric nature of retail banking, where employee retention directly impacts client relationships.

Dissimilarities in Risk Factors They Consider

Retail banks typically offer deposit accounts, loans, credit cards, and investment accounts. Meanwhile, commercial banking offers all of this, plus international banking, Treasury management, and more. Rayanne Harmon is a seasoned finance professional with 30 years of experience in banking, finance, and accounting. She specializes in consumer and business banking services, with deep expertise in credit products such as HELOCs, HELOANs, auto loans, and consumer loans.

The business imperative

This distinction highlights how ETFs in Diversified Banking Services can bridge gaps by offering tailored investment options for both individuals and businesses. Retail banking primarily serves individuals with personal financial products, while commercial banking focuses on providing specialized services to businesses and corporations. Retail banking offers services such as savings accounts, credit cards, and personal loans tailored to individual needs.

What Is The Difference Between Retail And Commercial Banking?

In summary, commercial banking is a vital part of the financial system, supporting the growth and development of businesses. By providing a range of specialized financial services and expert advice, commercial banks contribute to the success and stability of the business community. Commercial banks tend to focus on big corporations, mega projects, and affluent individuals with high net worth. Customers of any geographic area of the country can enjoy the services provided by the commercial banks as these services do not include day-to-day activities.

In addition to credit risk, commercial banks face market risk and operational risk. Market risk arises from fluctuations in interest rates, foreign exchange rates, and market prices of financial instruments. Commercial banks employ risk management techniques, such as hedging and diversification strategies, to mitigate market risks. Retail banking is the part of a bank that deals directly with individual, non-business customers. This operation brings in customer deposits that largely enable banks to make loans to their retail and business customers. Corporate, or business, banking deals with corporate and other business customers of varying sizes.

Foreign banks are established and operated from countries outside the US and often have operating branches stateside.

Retail bank employees receive medical insurance, retirement plans, and performance-based bonuses, which are designed to ensure financial security and enhance job satisfaction.

One of the primary services offered by retail banks is deposit and withdrawal transactions.

Commercial banking, on the other hand, has a substantially smaller transaction volume.

Retail vs Commercial Banking: Understanding the Differences

The main differences between retail banking and commercial banking are the type of products offered and the communities they serve. Retail banks and commercial banks differ significantly in the types of banking products they offer. These differences reflect the distinct needs of their respective customer bases and their specific financial goals. Additionally, retail banks often provide services such as financial planning, commercial and retail banking retirement planning, and insurance products to help customers secure their financial future. They serve as a trusted partner and offer financial advice tailored to the individual needs and goals of their customers. After that law was repealed in the late 1990s, corporate banking and investment banking services have been offered for many years under the same umbrella by most banks in the U.S. and elsewhere.

Commercial banks promote economic growth by infusing capital and building market liquidity. They circulate money from different bank customers through loans to help businesses expand their operations, provide more job opportunities, and create new products and services for general consumption. If you need commercial banking products and services, Bank of America is an excellent option.

Treasury and Cash Management Services

Professional service firms, such as law firms, consulting firms, and healthcare providers, are also important customers of commercial banks. These businesses may require financing for expansion, mergers and acquisitions, or to fund their professional services operations. Commercial banks offer tailored financial solutions to support the growth and success of professional service firms. Moreover, commercial banks offer treasury services to corporate clients, which involve managing their cash and liquidity positions, helping them optimize their investments, and mitigating financial risks. This includes providing foreign exchange services, managing interest rate risk, and advising on investment strategies to maximize returns. The operations of these two types of banks are not so similar, although both types do business through converting deposits into loans and other investments.

Primary Customer Base of Commercial Banks

Sign up to receive more well-researched small business articles and topics in your inbox, personalized for you. Commercial Banking, a private banking institution, literally means a bank engaged in commerce.

Retail loans typically involve smaller amounts and simpler structures, making them accessible for everyday financial goals like buying a car or funding education. For example, a home loan (also known as a mortgage) is a common retail banking product that enables individuals to purchase residential properties. The primary difference in education and certification between commercial and retail banking lies in their focus areas. Retail banking emphasizes customer service skills and product knowledge, while commercial banking prioritizes corporate finance expertise and credit management. Both sectors require foundational degrees but differ in specialized training programs and certifications. The table below highlights the key differences between retail and commercial banking, focusing on aspects such as target audience, primary focus, services offered, and customer satisfaction.

Equipment like this may be used in a range of industries, including manufacturing, information technology, and transportation. You also want to consider the possibility of “piercing the corporate veil” if you’re registered as a limited liability company or corporation. The risk of opening yourself up to liability by intermingling personal and business assets is too high. It makes it easier for you to track spending and income if you keep the two separated. In some banks, there are dedicated relationship managers, credit officers, and credit policies for each segment. Automated Teller Machine (ATM) technology has also advanced to provide a variety of services.

In contrast, commercial banks specialize in handling large-scale financial operations, supporting businesses with services like payroll processing and international trade financing. Retail banking primarily serves individual customers, commercial banking caters to businesses, and investment banking focuses on capital market activities. Retail banks provide personal financial services such as savings accounts, personal loans, and credit cards, addressing everyday monetary needs. These institutions prioritize accessibility and convenience for individual clients, ensuring financial stability at a personal level. On the other hand, commercial banking works more like a business coach, helping companies grow and handle large-scale financial operations.

In summary, the primary customer base of commercial banks comprises businesses, corporations, and large institutions with diverse financial needs. Commercial banks offer specialized financial services to support the growth, operations, and financial stability of these entities in various industries and sectors. In addition to lending, commercial banks offer trade finance services to facilitate international trade. They provide loans and lines of credit to businesses for various purposes, such as financing expansion plans, acquiring assets, managing cash flow, or funding working capital. These loans are tailored to the specific needs of the business, with terms and conditions based on the creditworthiness and risk profile of the borrower. For individuals seeking simplicity and ease of use, retail banks remain the preferred choice.

Their offerings, including personal savings accounts and household budgeting tools, are designed to build long-term relationships with individual clients. Unlike commercial banks, which handle complex corporate transactions, retail banks prioritize simplicity and accessibility for personal finance management. This distinction reflects the core purpose of retail banking in serving individual customers effectively. Retail banking offers personal financial services like savings accounts and credit cards, whereas commercial banking provides business-oriented services such as trade finance and cash management. Retail banks focus on simple transactions that cater to individual expenses, including everyday banking activities.

A company’s current ratio will often be higher than its quick ratio, as companies often use capital to invest in inventory or prepaid assets. For example, if a company has $1,000 in current liabilities on its balance sheet. But also has $1,500 in quick assets, so its quick ratio is 1.5, or $1,500 / $1,000. The quick ratio, also known as acid-test ratio, is a financial ratio that measures liquidity using the more liquid types of current assets. Its computation is similar to that of the current ratio, only that inventories and prepayments are excluded.

Part 2: Your Current Nest Egg

It is important to consider industry benchmarks and analyze the underlying factors contributing to the quick ratio.

However, a quick ratio of 1.0 is generally considered good, indicating that the company has as much in its most liquid assets as it owes in short-term liabilities.

A company with a healthy Quick Ratio is generally viewed as an attractive investment proposition, attracting more investors and potentially driving its market performance upwards.

Quick assets (cash and cash equivalents, marketable securities, and short-term receivables) are current assets that can be converted very easily into cash. The Quick Ratio is just one measure of liquidity, alongside the Current and Cash Ratios. The Current Ratio considers all current assets and liabilities, while the Cash Ratio measures a company’s ability to pay off its liabilities using only cash and cash equivalents.

Would you prefer to work with a financial professional remotely or in-person?

By analyzing a company’s liquidity, profitability, and solvency, investors can make more informed decisions about whether to invest in a particular company or not. Other factors such as long-term debt, profitability, and market trends should also be considered. Additionally, the Quick Ratio may vary by industry, with some industries requiring higher levels of liquidity than others. In conclusion, the quick ratio is a key liquidity metric that measures a company’s ability to meet its short-term financial obligations. It is important for analysts to consider when assessing a company’s overall health.

A Comparison of Acid-Test Ratio with Current and Cash Ratios

Because prepaid expenses may not be refundable and inventory may be difficult to quickly convert to cash without severe product discounts, both are excluded from the asset portion of the quick ratio. A company should strive to reconcile its cash balance to monthly bank statements received from its financial institutions. This cash component may include cash from foreign countries live basic full service 2020 translated to a single denomination. Unlock the potential of quick ratio with the comprehensive Lark glossary guide. For larger and more prominent companies, the Quick Ratio can act as a strategic tool to shape financial and corporate policies. By striving to maintain a consistently healthy Quick Ratio, these companies could be signalling their commitment to sustainable growth.

The current ratio, which simply divides total current assets by total current liabilities, is often used as a proxy for the quick ratio. While usually accurate, this approximation does not always represent the total liquidity of the firm. By excluding inventory, and other less liquid assets, the quick ratio focuses on the company’s more liquid assets. The quick ratio is an indicator of a company’s short-term liquidity position and measures a company’s ability to meet its short-term obligations with its most liquid assets. The quick ratio and the current ratio are both measures of a company’s liquidity, but they differ in the assets included. The quick ratio excludes inventory, while the current ratio includes inventory.

It measures the ability of a company to meet its short-term financial obligations with quick assets. The quick ratio does not include inventory, while the current ratio does, providing a less conservative, but more comprehensive, measure of a company’s liquidity. One benefit of the quick ratio is that it can provide a quick glimpse of a company’s financial status by comparing some of its most liquid assets to its liabilities.

It’s essential to consider industry norms and the company’s specific circumstances. A Quick Ratio of 1.0 or higher is generally considered healthy, indicating a company can meet its short-term obligations without selling inventory. In terms of accounts receivables, the quick ratio does not take into account the turnover rate or the average collection period. The quick ratio is a simple calculation that can be easily determined using the financial statements of a firm.

Accounts receivable, cash and cash equivalents, and marketable securities are some of the most liquid items in a company. And in a dynamic world, we have to supplement the financial statement given at a point in time with a trend analysis of changes that have occurred over time. It considers the fact that some accounts classified as current assets are less liquid than others.

It also does not provide information regarding the value of its inventory and marketable securities. Investors who are evaluating liquidity analysis using the quick ratio should keep a few things in mind. A higher quick ratio is generally better, as it points to a company that is more resilient and prepared to cover its short-term obligations. However, interested parties should keep in mind that a very high quick ratio may not be a positive development. There are also considerations to make regarding the true liquidity of accounts receivable as well as marketable securities in some situations.

These articles and related content is not a substitute for the guidance of a lawyer (and especially for questions related to GDPR), tax, or compliance professional. When in doubt, please consult your lawyer tax, or compliance professional for counsel. Sage makes no representations or warranties of any kind, express or implied, about the completeness or accuracy of this article and related content. When you leave a comment on this article, please note that if approved, it will be publicly available and visible at the bottom of the article on this blog. For more information on how Sage uses and looks after your personal data and the data protection rights you have, please read our Privacy Policy.

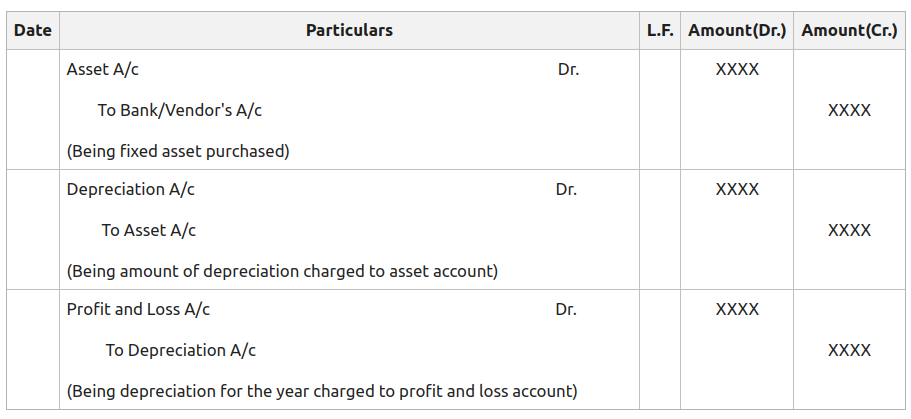

Hence, the credit balance in the account Accumulated Depreciation cannot exceed the debit balance in the related asset account. Depreciation expense is classified as a non-cash expense because the recurring monthly depreciation entry does not involve any cash transactions. As a result, the statement of cash flows, prepared using the indirect method, adds back the depreciation expense to calculate the cash flow from operations.

What Are Depreciation Expenses?

Accumulated depreciation is the total depreciation for a fixed asset that has been charged to expense since that asset was acquired and made available for use. The intent behind doing so is to approximately match the revenue or other benefits generated by the asset to its cost over its useful life (known as the matching principle). Depreciation expense is recorded on the income statement as an expense and reflects the amount of an asset’s value that has been consumed during the year. The four methods allowed by generally accepted accounting principles (GAAP) are the aforementioned straight-line, along with declining balance, sum-of-the-years’ digits (SYD), and units of production. Accumulated depreciation is the total amount of an asset’s original cost that has been allocated as a depreciation expense in the years since it was first placed into service.

Is Accumulated Depreciation an Asset or Liability?

As you can see, the accumulated depreciation account has a credit balance that increases over time. This is subtracted from the asset’s original cost to give you the net book value, which more accurately reflects the current value of the asset. Accumulated depreciation is recorded in a contra account, meaning it has a credit balance, which reduces the gross amount of the fixed asset. Depreciation expenses a portion of the cost of the asset in the year it was purchased and each year for the rest of the asset’s useful life. Accumulated depreciation allows investors and analysts to see how much of a fixed asset’s cost has been depreciated.

To put it simply, accumulated depreciation represents the overall amount of depreciation for a company’s assets, while depreciation expense refers to the amount that has been depreciated in a specific period.

Accumulated depreciation is a real account (a general ledger account that is not listed on the income statement).

Otherwise, only presenting a net book value figure might mislead readers into believing that a business has never invested substantial amounts in fixed assets.

Hence, the credit balance in the account Accumulated Depreciation cannot exceed the debit balance in the related asset account.

A typical presentation of accumulated depreciation appears in the following exhibit, which shows the fixed assets section of a balance sheet.

Why does accumulated depreciation have a credit balance on the balance sheet?

Various methods, such as straight line, declining balance, sum-of-the-years’ digits, and units of production, are used to calculate depreciation. It is credited each year as the value of the asset is written off and remains on the books, reducing the net value of the asset, until the asset is disposed of or sold. Depreciation expense is considered a non-cash expense because the recurring monthly depreciation entry does not involve a cash transaction.

Unlike a normal asset account, a credit to a contra-asset account increases its value while a debit decreases its value. Depreciation expense is recorded on the income statement as an expense or debit, reducing net income. Instead, it’s recorded in a contra asset account as a credit, reducing the value of fixed assets. Depreciation expenses, on the other hand, are the allocated portion of the cost of a company’s fixed assets for a certain period. Depreciation expense is recognized on the income statement as a non-cash expense that reduces the company’s net income or profit.

Double-Declining Balance Method

However, there are situations when the accumulated depreciation account is debited or eliminated. Depreciation is defined as the expensing of an asset involved in producing revenues throughout its useful life. Depreciation for accounting purposes refers the allocation of the cost of assets to periods in which the assets are used (depreciation with the matching of revenues to expenses principle).

To put it another way, accumulated depreciation is the total amount of an asset’s cost that has been allocated as depreciation expense since the asset was put into use. If an asset is sold or disposed of, the asset’s accumulated depreciation is “reversed,” or removed from the balance sheet. Because a fixed asset does not hold its value over time (like cash does), it needs the carrying value to be gradually reduced. Depreciation expense gradually writes down the value of a fixed asset so that asset values are appropriately represented on the balance sheet.

The initial accounting entries for the first payment of the asset are thus a credit to accounts payable and a debit to the fixed asset account. Each year, the depreciation expense account is debited, expensing a portion of the asset for that year, while the accumulated depreciation account is credited for the same amount. Over the years, accumulated depreciation increases as the depreciation expense is charged against the value of the fixed asset.

Physical assets, such as machines, equipment, or vehicles, degrade over time and reduce in value incrementally. Unlike other expenses, depreciation expenses are listed on income statements as a “non-cash” charge, indicating that no what does the credit balance in the accumulated depreciation account represent money was transferred when expenses were incurred. Let’s assume that a retailer purchased displays for its store at a cost of $120,000. By having accumulated depreciation recorded as a credit balance, the fixed asset can be offset.

It is calculated by summing up the depreciation expense amounts for each year up to that point. Since accumulated depreciation is a credit entry, the balance sheet can show the cost of the fixed asset as well as how much has been depreciated. From there, we can calculate the net book value of the asset, which in this example is $400,000. Accumulated depreciation is dependent on salvage value; salvage value is determined as the amount a company may expect to receive in exchange for selling an asset at the end of its useful life.

(4) Analysis of any variances and to ascertain the reasons of such variation. (5) To apply the principle of ‘management by exception’ at operational level. (1) To develop forward looking and onward looking approach at each level of management. (iv) To motivate operating and managerial personnel in the direction of improved efficiency. F) Standard costing simplifies bookkeeping, as information is recorded at standard, instead of a number of historic figures. (d) Deciding on the appropriate mix of component materials, where some change in the mix is possible.

Not Suitable for Fast-Paced Environments with Regular Price Fluctuation

Since a manufacturer must pay its suppliers and employees the actual costs, there are almost always differences between the actual costs and the standard costs, and the differences are noted as variances.

To be meaningful, while quantity standards should not be revised frequently, price standards essentially require periodic revision.

As a result, this is an unfavorable variable manufacturing overhead efficiency variance.

(5) To apply the principle of ‘management by exception’ at operational level.

That part of a manufacturer’s inventory ledger account that is in the production process but not yet completed. This account contains the cost of the direct material, direct labor, and factory overhead in the products so far. A manufacturer must disclose in its financial statements the cost of its work-in-process as well as the cost of finished goods and materials on hand.

Normal Standards

Another objective is to implement a feedback control cycle within a business. Unless the manufacturing process is complete, it is not possible to accurately predict the production costs and other expenses. Bookkeeping for Painters Several unknown variables like an increase in the cost of raw material, changing labour costs, interruptions and delays in production, and others have an effect on the final cost of the finished product.

Advance Your Accounting and Bookkeeping Career

In a standard costing system, the costs of production, inventories, and the cost of goods sold are initially recorded using the standard costs. In the case of direct materials, it means the standard quantity of direct materials that should have been used to make the good output. If the manufacturer uses more direct materials than the standard quantity of materials for the products actually manufactured, the company will have an unfavorable direct materials standard costing usage variance. Standard costing should be used in situations where a business engages in repetitive manufacturing processes with predictable and consistent costs. It is particularly effective for companies that produce large volumes of standardized products, as it simplifies budgeting, cost control, and variance analysis.

Problems in Setting Standard Costs

The differences of actuals and standards may be taken to variance accounts. Standard cost is a planned cost for a unit of product, component or service produced in a period. Standard costing is introduced primarily to ascertain the efficiency of cost performance. Accordingly, standard costing is a tool or technique of cost control.

It is also useful for the manager since a complete assessment of the performance for a certain period can be carried out. It allows you to understand what mistakes were made and what should be done to achieve greater efficiency. Founded in 2017, Acgile has evolved into a trusted partner, offering end-to-end accounting and bookkeeping solutions to thriving businesses worldwide. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

The next step after preparing an Adjusted Trial Balance would be the closing process.

It makes sure statements like the cash flow are accurate and truly represents the company’s financial health.

By verifying the equality of debits and credits, the post-closing trial balance confirms that the accounts are ready for the next accounting period.

Accounting software will generate a post-closing trial balance (or any other trial balance) with a click of the mouse.

Since these are determined to be temporary accounts, it contains no sales revenue entries, expense journal entries, no gain or loss entries, etc.

Post-Closing Trial Balance Vs. Adjusted Trial Balance:

The last step in the accounting cycle (not counting reversing entries) is to prepare a post-closing trial balance. They are prepared at different stages in the accounting cycle but have the same purpose – i.e. to test the equality between debits and credits. The General Ledger Trial Balance Report lists actualaccount balances and activity by ledger, balancing segment, and accountsegment. The report prints the account number, description, and debitor credit balance for the beginning and ending period. The report can print incomestatement, balance sheet, or all balances for a selected range ofaccounting combinations.

AccountingTools

First, identify the accounts that possess balances, and if closing entries were performed correctly, these should simply be those on your company’s balance sheet. It helps to prepare your general ledger for the new accounting period and closes out balances in both expenses and revenue accounts. While it differs from an adjusted trial balance in purpose and content, both serve as crucial tools to ensure the accuracy of financial records and statements. These accounts carry their balances into the next accounting period and are used to prepare the financial statements. However, most businesses can streamline this cycle and skip tedious steps like posting transactions to the general ledger and creating a trial balance. Using accounting software like QuickBooks Online can do all these tasks for you behind the scenes.

Streamline your accounting and save time

Post Closing Trial Balance is the list of all the balance sheet items and their balances, excluding the zero balance accounts. It is used for verification that temporary accounts are properly closed and that the total balances of all the debit accounts and all the credit accounts are equal. A post-closing trial balance is, as the term suggests, prepared after closing entries are recorded and posted. It is the third (and last) trial balance prepared in the accounting cycle. The balances of the nominal accounts (income, expense, and withdrawal accounts) have been absorbed by the capital account – Mr. Gray, Capital.

Role in Verifying Accounting Accuracy

As with the unadjusted and adjusted trial balances, both the debit and credit columns are calculated at the bottom of a trial balance. If these columns aren’t equal, the trial balance was prepared incorrectly or the closing entries weren’t transferred to the ledger accounts accurately. In financial reports, this balance confirms account balances are mathematically correct after closing entries. It makes sure all temporary accounts are cleared, fitting accounting standards. This step keeps the financial statements truthful, including balance sheets and income statements. In both adjusted and unadjusted trial balances, the total of both credit and debit is calculated at the bottom of the trial balance, and they should be equal.

Deferred Tax Assets – Definition, Example, and Why the Deferred Tax Asset Arises

After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. Specify the currency type, such as entered, statistical,or total. For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

A trial balance is an internal report that itemizes the closing balance of each of your accounting accounts. It acts as an auditing tool, while a balance sheet is a formal financial statement. It’s one of the first lines of defense against accounting errors and a pivotal report within double-entry bookkeeping.

It’s vital for the adjusted trial balance, pre-closing trial balance, and post-closing trial balance. Knowing their differences improves the value of financial statements. This is to ensure things like dividends are correctly taken from net income.

Temporary accounts are used to record transactions for a specific accounting period, such as revenue, expense, and dividend accounts. A trial balance only contains ending balances of your accounting accounts, while the general ledger has detailed transactions of the accounts. Most accounting software will let you generate a trial balance at any point in time to allow you can i get a tax refund with a 1099 even if i didn’t pay in any taxes to assess the current state of your accounts. Instead, they are accounting department documents that are not distributed. In the next accounting period, the accounting cycle will be repeated again starting from the preparation of journal entries i.e. the first step of accounting cycle. Keeping accurate financial records keeps communication with stakeholders clear.